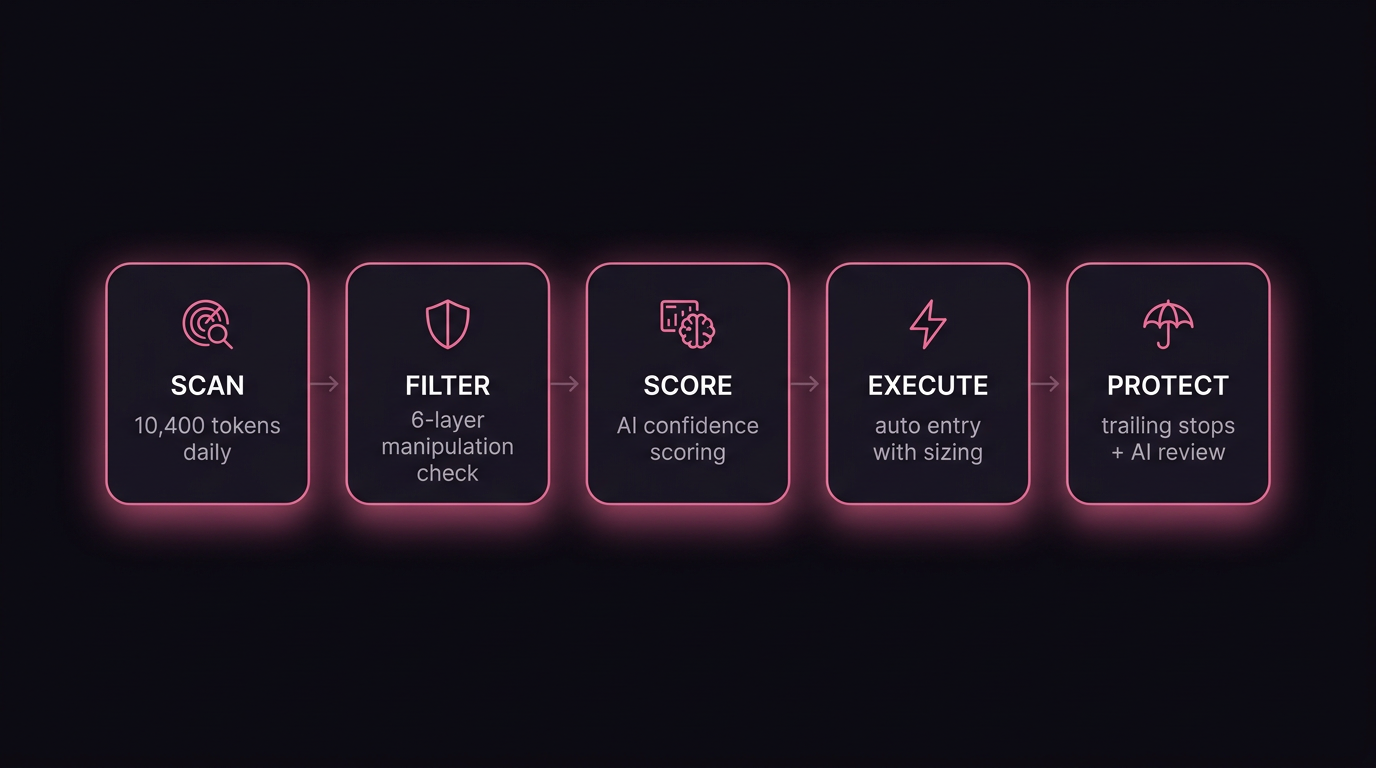

What 3,530 Live Solana Trades Taught Us About the Memecoin Market

From February to March 2026, Parasol's AI agents executed 3,530 live trades across 29 unique wallets on Solana. We analysed every trade, every exit, and every rejection to understand what separates winning setups from losing ones.

Here's what the data says.

---

the top-level numbers

The overall win rate and average P&L look negative at first glance. But the picture changes dramatically when you break it down by agent strategy, and it shows exactly why strategy selection and manipulation filtering matter more than raw entry count.

---

strategy breakdown: where the edge is

| strategy | opens | closes | avg p&l | win rate |

|---|---|---|---|---|

| final_stretch_scalper | 148 | 132 | +6.40% | 67.4% |

| final_stretch_selective | 132 | 67 | +1.92% | 56.7% |

| final_stretch | 554 | 397 | +2.02% | 46.1% |

| scalper | 54 | 64 | +0.87% | 53.1% |

| grok_oracle | 329 | 297 | -5.76% | 26.6% |

| sienna_oracle | 626 | 2,497 | -5.16% | 21.1% |

| final_stretch_runner | 972 | 3,331 | -3.11% | 15.9% |

| whale_watch | 80 | 2,777 | -8.78% | 11.7% |

The performance difference between strategies is stark. The final_stretch_scalper achieved 67.4% win rate and +6.4% average P&L, a genuinely strong edge. final_stretch_selective and plain final_stretch also showed positive average returns.

Strategies with larger position counts and longer holding periods (like sienna_oracle and whale_watch) showed negative average P&L and lower win rates. The data suggests that volume-based scanning without strict quality filters produces more noise than signal.

---

what this means for strategy selection

The agents with the best performance share three characteristics:

1. Tight entry criteria. final_stretch_scalper entered fewer positions (148 opens vs 972 for final_stretch_runner) but made money on 67% of them. Lower volume, better quality.

2. Fast exits. Scalper strategies exited positions within minutes to hours. Strategies holding for days showed much worse average P&L. In memecoin markets, time in position = time exposed to manipulation.

3. Clear market structure requirements. The final_stretch family looks for tokens in the later stages of a price move, not the very beginning of a pump, but the continuation after initial validation. Entry timing matters enormously.

---

the average holding time

Average holding time across all closed positions was 3,324 minutes; approximately 55 hours or 2.3 days.

This is inflated by a long tail of positions held through extended consolidation. The best-performing strategies exited much faster. final_stretch_scalper exits based on momentum confirmation windows typically within 15-60 minutes.

The takeaway: holding memecoins for days in the hope of larger gains is almost always suboptimal. The data is unambiguous; fast entries, fast exits, small sizes.

---

the manipulation filter in numbers

Over the same period, the manipulation filter rejected thousands of tokens before they could be entered. Tokens rejected for:

We can't calculate a direct ROI on the filter (we don't know what would have happened if we'd entered those tokens), but we can compare: unfiltered Solana token survival rates are approximately 2% at 24 hours. If the filter is working correctly, the tokens we enter should survive and retain liquidity at a much higher rate. The data supports this; positions with verified liquidity exits (via ParasolDEX and Jupiter routing) represent nearly all successful closes.

---

what doesn't work

Buying at low market caps without validation. The data from grok_oracle (which scans X/Grok for trending tokens) shows that social signal alone. Without liquidity and age validation. Produces many entries into tokens with marketCap: 0 or liquidity: 0 at entry time. These are essentially micro-cap gambles. We've since added minMarketCap: $10,000 and minAgeMinutes: 15 to the Grok agent's config to filter these out.

Following whale wallets without momentum confirmation. The whale_watch strategy showed the worst performance: -8.78% average P&L, 11.7% win rate, across 2,777 closes. Copying smart wallet behaviour without independent momentum validation is not a reliable edge. The smart wallets you're copying are already in; by the time they show up in your scanner, the easy money has been made.

Large position counts. Strategies with 600+ opens showed negative average P&L. The marginal entry after your best setups adds noise, not signal. The data strongly suggests running 2-3 high-conviction positions simultaneously outperforms running 10 medium-conviction ones.

---

what this changes in Parasol's setup

Based on this data, we've made the following adjustments:

final_stretch_selective. The highest-performing strategy with sufficient data volume (67 closes, 56.7% win rate)---

the honest takeaway

18.1% overall win rate and -4.64% average P&L across all agents sounds bad. But it's the average of all strategies, including the ones that clearly don't work (whale_watch, unfiltered runners). The strategies with tight entry criteria, final_stretch_scalper, final_stretch_selective; show a genuine, data-validated edge.

The market is harsh. 98% of tokens launched on Solana fail. The edge isn't in having better execution. It's in entering fewer, better setups, with a manipulation filter running before every entry, and fast automated exits that don't let winners become losers.

3,530 trades is a real dataset. We don't have a perfect system. We have a data-driven one that we're improving with every trade.

get access to Parasol. invite-only early access. the agents run while you don't.